In this special episode of THE SAMPLE, Leita Hart-Fanta, CPA talks to Charles Hall, CPA about how to report Yellow Book findings.

Blog

Scope: The Boundary of Your Audit

Scope is the boundary and one of three main parameters of your audit with the audit objective and methodologies making up the other two.

COSO vs. GAGAS

In 2018, the GAO asked us to evaluate the auditee against the COSO model of internal controls. Now in 2024, the GAO is asking us to apply COSO concepts to our own audit organization. Karma!

The New Quality Management Standards

In this special episode of THE SAMPLE, Leita Hart-Fanta, CPA talks to Charles Hall, CPA about the new Quality Management Standards.

3 Roles on an Audit Engagement

GAGAS section 4.10 reminds us professional maturity depends on our ability to tolerate uncertainty and ambiguity. The 3 roles on an audit engagement generally include non-supervisory auditors, supervisory auditors and partners/directors.

Colin Powell’s Rules for Evidence

In a 2014 book, former Secretary of State Powell explained how he judges evidence and where he went wrong with his speech to the UN on Iraq’s weapons of mass destruction. These same principles apply to audit evidence.

Risk Assessment: Performance Audits vs. Financial Audits

In this special episode of THE SAMPLE, Leita Hart-Fanta talks to Charles Hall about risk assessment by comparing performance and financial audits.

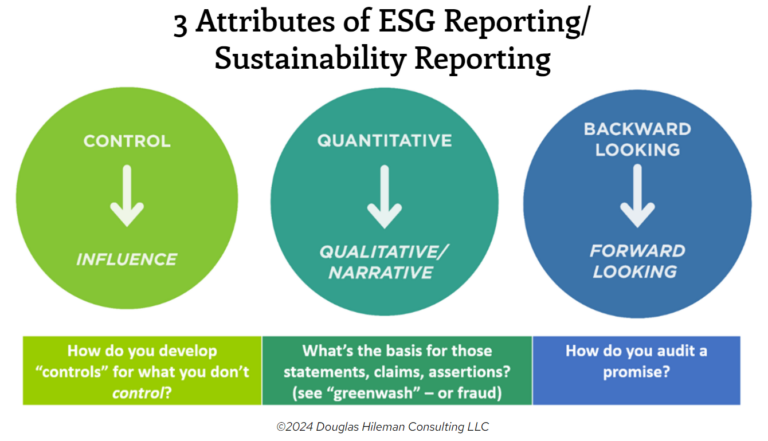

3 Attributes of ESG Reporting

Featured speaker, Douglas Hileman, shares how government entities play an important role in ESG reporting. Government promulgates regulations, develops policies, manages programs, and may have monitoring and enforcement authority over business partners and regulated entities. So much to know!

Linkage: How Audit Objectives, Risk, Findings & Evidence Fit Together

Always make sure the major parts of the audit fit together. The objective is satisfied, and the risks are addressed. The findings address the objective and the risks while supported by evidence… Linkage!

Yellowbook-CPE.com is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website:

Yellowbook-CPE.com is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website: