The GAGAS 2023 exposure draft proposes an audit leader reaches one of three conclusions after their annual internal assessment of quality.

Blog

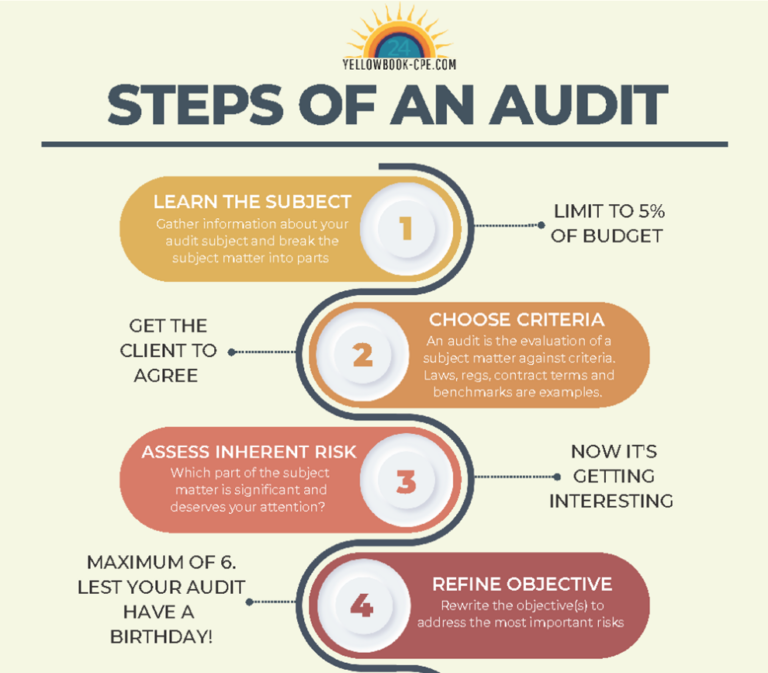

Steps of an Audit

From the simplest to the most complex audits, Leita Hart-Fanta provides the Steps of an Audit as a guide for auditors on their future assignments.

Response to the 2023 Exposure Draft of GAGAS

In a letter to the GAO, Leita Hart-Fanta addresses multiple inconsistencies in the Yellow Book, including comments on the 2023 exposure draft of GAGAS.

The Proposed Quality Management Risk Assessment Process

The 2023 GAGAS exposure draft proposes a three-step quality management risk assessment process so your team conducts better audits.

The GAO wants us to think about Audit Quality

The 2023 GAGAS exposure draft proposes auditors apply a formal three-step process to protect audit quality.

Audit Room Podcast Ep 37: Wait, There’s a Yellow Book, too?

Leita Hart-Fanta was recently a guest on The Audit Room, the number one podcast where auditors can share their experiences, ask questions and get expert coaching and feedback. Listen now!

What Is Segregation of Duties?

In this episode of THE SAMPLE Leita Hart-Fanta shares examples that show clearly what segregation of duties is not. What is segregation of duties?

Safeguards to Independence

One of the best safeguards to independence is to withdraw from the audit engagement entirely. Fortunately, that’s not the only solution.

Who Says There’s No Free Lunch? Free FASB and GASB Access

Here’s some good news if you perform accounting work in the United States: Free access to FASB and GASB information!

Yellowbook-CPE.com is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website:

Yellowbook-CPE.com is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website: