In 2018, the GAO asked us to evaluate the auditee against the COSO model of internal controls. Now in 2024, the GAO is asking us to apply COSO concepts to our own audit organization. Karma!

Gao green book

Audit Room Podcast Ep 37: Wait, There’s a Yellow Book, too?

Leita Hart-Fanta was recently a guest on The Audit Room, the number one podcast where auditors can share their experiences, ask questions and get expert coaching and feedback. Listen now!

What Is Segregation of Duties?

In this episode of THE SAMPLE Leita Hart-Fanta shares examples that show clearly what segregation of duties is not. What is segregation of duties?

How to Fight the Bureaucracy

In this episode of THE SAMPLE, Leita Hart-Fanta, CPA discusses how to fight the bureaucracy.

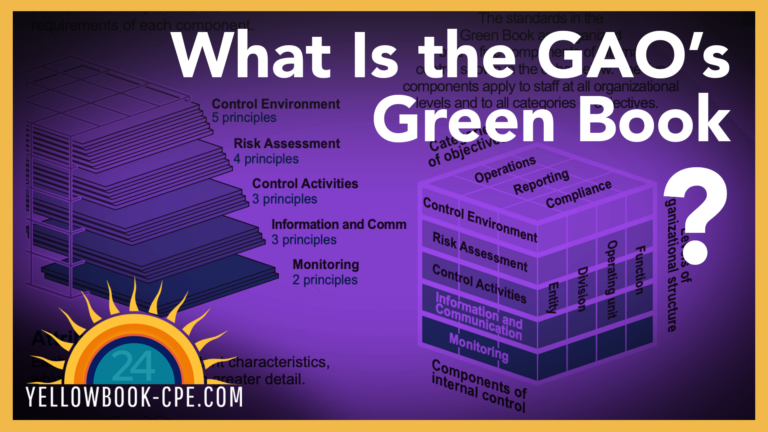

What Is the GAO Green Book?

In this episode of THE SAMPLE, Leita Hart-Fanta, CPA answers the question, “What is the GAO’s Green Book?” The Green Book’s formal title is Standards for Internal Control in the Federal Government and is a close copy of the COSO model.

Yellowbook-CPE.com is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website:

Yellowbook-CPE.com is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website: