The GAO’s 2025 Green Book is out! It reminds us controls aren’t just about compliance. It’s about being a good steward of public resources, achieving mission objectives, and earning the public’s trust.

Audits

Streamline Your Audit Report Writing Using a 9-Step Process

Streamline your audit report writing process by sticking to a simple 9-step process taking the team through planning, drafting, editing, and formatting.

Audit Resources for Smooth Sailing

Running an audit organization is like captaining a ship. With the right crew, enough provisions, and a clear course, you’ll navigate the seas of risk with confidence.

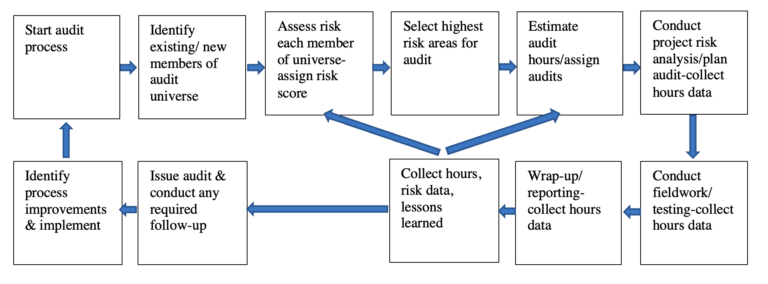

Continuous Improvement Tools for Better Audits

Special thanks to Alfredo Mycue and Susan Oballe for this valuable article on continuous improvement tools for government auditing.

Internal Audit KPI Metrics to Rock Your Audit Shop

Do you manage your audit projects or do they manage you? Internal Audit KPI metrics help you manage your projects, audit team and risk to rock your audit shop!

Truth Telling Power

Does your audit organization have truth telling power with clear guidelines, the right spot in the organizational chart and access to all the data?

Integrating Cybersecurity with Governance, Risk Management & Compliance

Featured speaker, Joe Horowitz, shares his cybersecurity expertise on bridging the gap between governance, risk management and compliance practices to enhance organizational security.

3 Roles on an Audit Engagement

GAGAS section 4.10 reminds us professional maturity depends on our ability to tolerate uncertainty and ambiguity. The 3 roles on an audit engagement generally include non-supervisory auditors, supervisory auditors and partners/directors.

Colin Powell’s Rules for Evidence

In a 2014 book, former Secretary of State Powell explained how he judges evidence and where he went wrong with his speech to the UN on Iraq’s weapons of mass destruction. These same principles apply to audit evidence.

Yellowbook-CPE.com is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website:

Yellowbook-CPE.com is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website: