The elements of an audit finding are so core to planning, performing, and reporting on an audit, one newsletter can only scratch the surface on all that needs to be said! In this newsletter, we will just get a sense of what the elements of an audit finding are.

What are the elements of a finding?

There are five elements of a finding:

- condition

- effect

- cause

- criteria

- recommendation

Where did these “elements of a finding” come from?

Greek philosophers outlined the elements of a persuasive argument centuries ago.

Some smarty pants (and I say that in a complimentary way!) at the GAO (Government Accountability Office) was wise enough to include the elements of a persuasive argument in the Yellow Book (Generally Accepted Government Auditing Standards) and rename them as the elements of a finding.

The IIA also recommends that auditors use the elements of an audit finding in order to make audit findings as transparent and convincing as possible.

Strangely enough, the AICPA is silent on what should be included in a management letter comment or as many auditors call them, audit findings. In my opinion, this is one of the major weaknesses in the AICPA’s Statements on Auditing Standards … but they didn’t ask me!

Why bother with the elements of an audit finding?

The Greeks and the smarty pants at the GAO realized that there are a few key pieces of information that everyone needs to know about an audit issue.

Each of the five elements has a purpose—clears something up for the reader—and should not be left out. If you leave an element out, you leave the reader hanging and pondering unanswered questions.

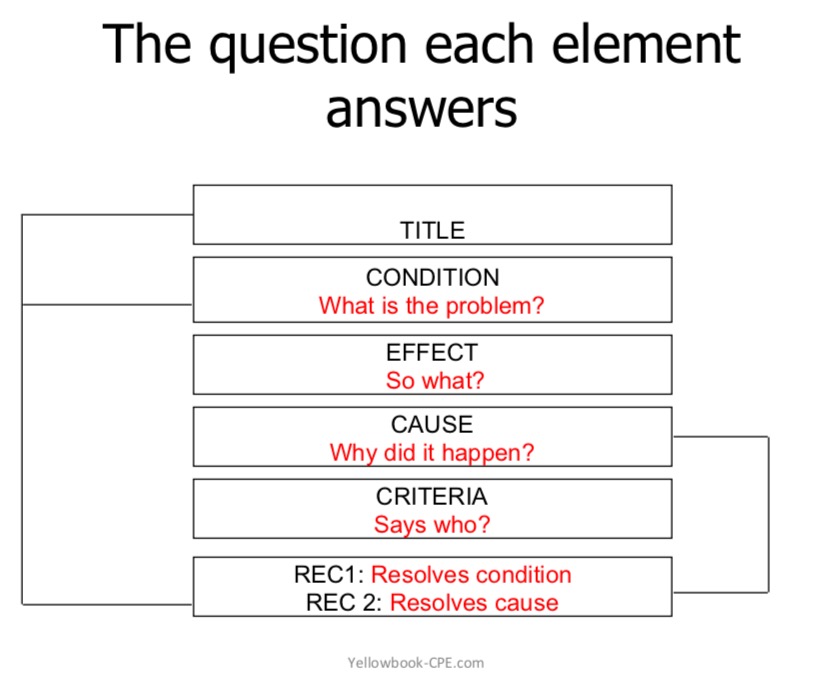

What questions do the elements of an audit finding answer for the reader?

- Condition: What is the problem/issue? What is happening?

- Effect: So what? Why should the reader care about this condition? What is the impact?

- Cause: How or why did the condition happen?

- Criteria: Says who? Who says this is a problem?

- Recommendation 1: How do we resolve the condition?

- Recommendation 2: How do we resolve the cause?

A few rules about using the elements

- Use only one of each. For each finding, choose only one sentence to represent each of the elements. This will keep your audit finding tight and ensure logical organization. If you add several conditions, effects, or causes, you will confuse and lose the reader and probably yourself, too!

- The elements must match. There are two recommendations. One to match the condition and one to match the cause. In other words, the recommendation must resolve the two problems you raised, both the condition and the cause. To make your argument very clear, use the same terminology in the condition and the cause that you do in the recommendation. Image of how the elements match

For example, let’s say that you are auditing a school lunch program and you find that approximately 5% of the kids who receive free lunch are not eligible. The finding might look like this?

- Condition: Ineligible students are receiving free lunch

- Effect: 6 out of 120 students tested were not eligible resulting in $X of questioned costs

- Cause: Admin not screening for eligibility

- Criteria: Federal grant requirements say….

- Recommendation 1: Ensure only eligible students receive free lunch

- Recommendation 2: Admin screens students for eligibility

Notice that the terminology used in the recommendation mirrors or matches the terminology in the condition and cause. Also notice that at this point we are not creating full sentences. Don’t invest time in crafting full sentences until you are happy with the outline. We will work with this audit finding more in future newsletters.

Want to learn more about how to write a finding? Check out this on demand video here: https://yellowbook-cpe.com/product/art-of-the-finding-video

Yellowbook-CPE.com is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website:

Yellowbook-CPE.com is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website: