It seems like everyone is always crunched for time and “busy” these days. As auditors, we can save our readers a few moments of precious time. How you ask? By writing executive summaries, of course!

The executive summary highlights the most important information from the longer, more detailed report. We want to ensure our audience walks away with an audit overview and a few major ideas.

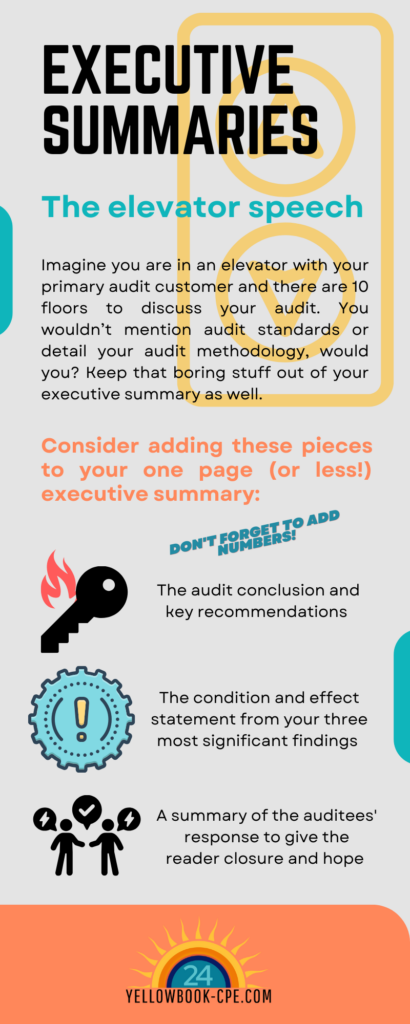

What’s included in executive summaries?

To get the best bang for your reader’s buck, I recommend having these in every executive summary:

- A highlight of the two or three most important issues and recommendations

- A description of the significance of the issues and of the audit report

- A summary of the client’s response to the recommendations

- A summary of the audit objective and scope

I know you’re super excited about your well-written report, but don’t send it just yet! Ask yourself the below questions prior to sending the final version to your readers:

Does it address the needs and concerns of decision makers?

Your audience often includes high-level decision makers and one of their most fundamental needs is brevity. So, the executive summary should be as short as possible with one page or less as the ideal length.

Does the detailed section mirror the executive summary?

The sequence of items in the detailed section must match the same order in the executive summary. Otherwise, the reader of the executive summary may become frustrated wading through the detail trying to pick up more information on important issues. Understandably, audit reports can be complicated and this is your chance to clarify your message.

Will it encourage reading the detailed section?

Some think of the executive summary of an audit report as just a teaser, or something to entice the reader to open up the full detail. To intrigue your readers to delve deeper, the executive summary can quantify or state dollars with significant issues. Additionally, an enticing executive summary includes action titles and points directly to major issues.

Are the impact and significance of issues clearly stated?

Do the issues sound theoretical or real? Is the language concrete or academic?

- Academic: Controls over cash should be improved.

- Concrete: The accounting department does not perform cash reconciliations each month.

Sometimes, in order to save space, we cut too many words or generalize until our writing is mush. State it plainly with concrete terminology.

Are issues quantified?

You can quantify the error, issue or area audited. For example:

- Error: 5 checks bounced costing the entity $250 in bank fees.

- Issue: The bank account processes 400 transactions a month and averages a balance of $1M.

- Area: The bank account tracks disbursements of the entity’s largest grant, the Peters Grant. The Peters Grant distributes $150 million dollars to sub-recipients each year.

Is the executive summary “balanced?”

The executive summary should present an objective and fair view. Avoid judgmental language, such as poor, weak and inadequate. Surely that’s easy to do if you simply stick with the facts. Also, don’t make a mountain out of a molehill. Besides, if everything is fine except for a few minor issues, go ahead and say so.

Yellowbook-CPE.com is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website:

Yellowbook-CPE.com is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website: