From the windswept Great Plains comes a tale of bravery, integrity, and justice. Joshua Gallion is the auditing superhero on this week’s episode of the “Auditors Save the World” podcast!

performance audit

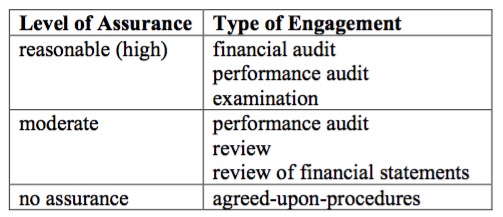

5 Engagement Types Per GAGAS

Under Yellow Book standards, an auditor can perform 1 of 5 engagement types: financial audit, performance audit, examination, review and agreed-upon procedures.

Risk Assessment: Performance Audits vs. Financial Audits

In this special episode of THE SAMPLE, Leita Hart-Fanta talks to Charles Hall about risk assessment by comparing performance and financial audits.

Descriptive Performance Audits?

According to GAGAS, what’s the difference between a descriptive performance audit and an evaluative performance audit? Don’t know? Find out now!

What is the purpose of a performance audit?

In this episode of THE SAMPLE, Leita Hart-Fanta, CPA answers the question, “What is the purpose of a performance audit?”

Performance Audit vs. Financial Audit

So how do you tell the difference? Performance audit vs. financial audit? You might expect that it would be as simple as saying that a financial audit deals with money and a performance audit does not. But oh no! The audit standards are never that straightforward. As a matter of fact, the most comprehensive audit […]

Do I need an audit, a review, or a monitoring visit? What is the difference?

If you have doubts that your audit customer understands what you do and how important you are 🙂 , share this article with them: Plenty, my friend! Plenty. So, you think you need an audit? Or maybe you heard that you could get by with a review instead? Maybe you were asked to find someone […]

Executive Summaries for Performance Audit Reports

Using executive summaries cuts through the details of a performance audit so your reader gets to the main message fast!

Yellowbook-CPE.com is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website:

Yellowbook-CPE.com is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website: