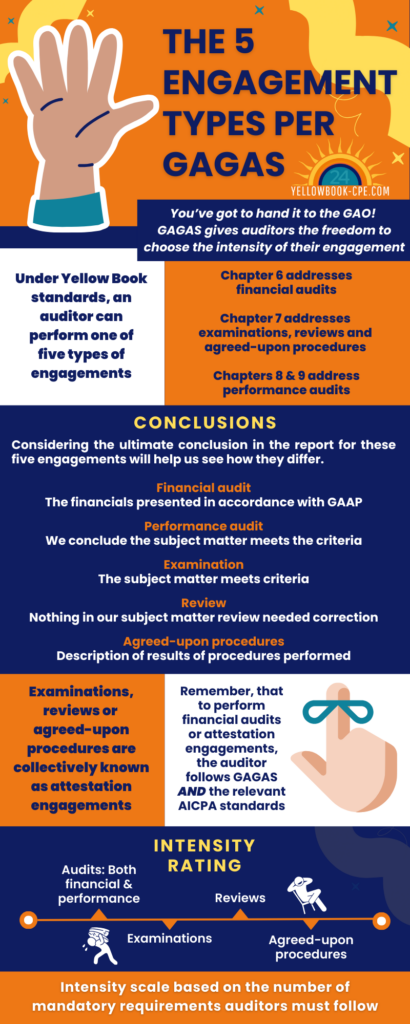

The 5 Engagement Types Per GAGAS

You’ve got to hand it to the GAO!

GAGAS gives auditors the freedom to choose the intensity of their engagement.

Under Yellow Book standards, an auditor can perform one of 5 engagement types:

- Chapter 6 addresses financial audits

- Chapter 7 addresses examinations, reviews and agreed-upon procedures

- Chapters 8 & 9 address performance audits

Conclusions

Considering the ultimate conclusion in the report for these five engagements will help us see how they differ.

- Financial audit: The financials presented in accordance with GAAP

- Performance audit: We conclude the subject matter meets the criteria

- Examination: The subject matter meets criteria

- Review: Nothing in our subject matter review needed correction

- Agreed-upon procedures: Description of results of procedures performed

Examinations, reviews or agreed-upon procedures are collectively known as attestation engagements.

Remember, that to perform financial audits or attestation engagements, the auditor follows GAGAS AND the relevant AICPA standards.

Intensity rating

The more requirements necessary, the more intense the engagement.

Both financial and performance audits must follow much more stringent guidelines than agreed-upon procedures.

Want to learn more?

Join Leita for the 8-hour live webinar, Yellow Book Standards for Performance Auditors, on November 13-14.

This course highlights the crucial updates performance auditors need to know, including independence, CPE requirements, and the latest on quality control and peer review. Also, we’ll also ground ourselves regarding GAGAS requirements regarding internal controls!

Performance auditors will learn the major and minor themes of the engagement chapters as well as new terms and definitions added to the latest Yellow Book.

Yellowbook-CPE.com is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website:

Yellowbook-CPE.com is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website: