Special thanks to John J. Hall, CPA, President, Hall Consulting, Inc. for providing this valuable information on internal control.

Internal Controls

5 Strong Controls

Is there a risk you want to avoid? Of course there is! Apply these 5 strong controls today to reduce your chance at risk.

31+ Movies to Sharpen Your Professional Skepticism

Auditors! Grab some popcorn and watch these movies to become better at detecting corruption and fraud.

How to Fight the Bureaucracy

In this episode of THE SAMPLE, Leita Hart-Fanta, CPA discusses how to fight the bureaucracy.

How Do I Teach My Clients About Internal Controls?

In this episode of THE SAMPLE, Leita Hart-Fanta, CPA answers the question, “How Do I Teach My Clients About Internal Controls?” Does your auditee recognize that they are responsible for internal controls? Leita shares tips on how to introduce your client to the COSO model without overwhelming them.

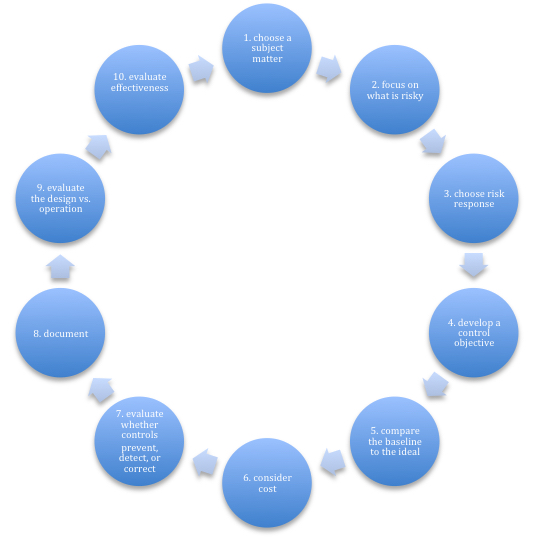

Where There Is Risk There Must Be Choice

In this episode of THE SAMPLE, Leita Hart-Fanta, CPA discusses the connection of Risk and Choice and what to do with an inherent risk once identified.

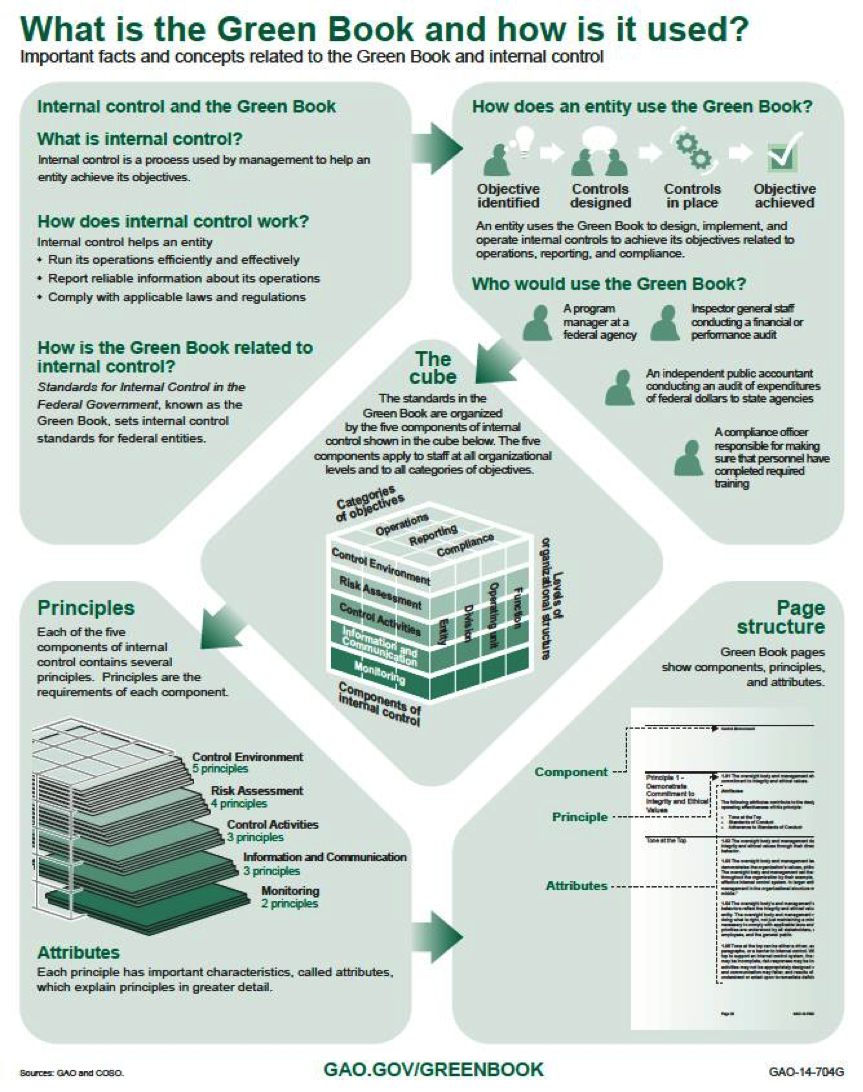

The Most Important Change to the Yellow Book is the Green Book

I’ve had a few months to digest the changes to the 2018 Yellow Book (Government Auditing Standards),and I’ve taught a few seminars and webinars about the changes. Most of the changes do not shock my audiences. But I am noticing that quite a few auditors are not familiar with the Green Book which was published by […]

Pulling It All Together

What’s the matter with the crowd I’m seeing? “Don’t you know that they’re out of touch?” Should I try to be a straight-A student? “If you are then you think too much. Don’t you know about the new fashion, honey? All you need are looks and a whole lot of money?” It’s the next phase, […]

2018 GAO Yellow Book Revisions

The 2018 GAO Yellow Book revisions are out and the biggest addition is the Green Book, which is all about internal controls. Are you ready?

Yellowbook-CPE.com is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website:

Yellowbook-CPE.com is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website: