Make your audit reports more dynamic by using parallelism: Similar words, phrases, bulleted lists and other grammatical elements to emphasize similar ideas in a sentence.

Financial

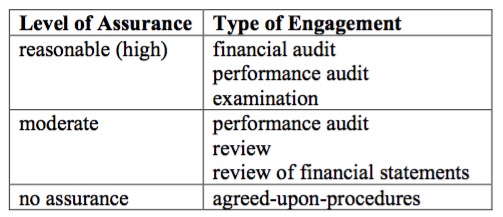

Performance Audit vs. Financial Audit

So how do you tell the difference? Performance audit vs. financial audit? You might expect that it would be as simple as saying that a financial audit deals with money and a performance audit does not. But oh no! The audit standards are never that straightforward. As a matter of fact, the most comprehensive audit […]

Yellowbook-CPE.com is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website:

Yellowbook-CPE.com is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website: